Pooja Choudhary

FinTech, or financial technology, is a term used to describe any new technology that channelizes to improve and automate the use and delivery of financial products and services. Below are the major 6 key parts of the Fintech industry into which this technology is basically divided. Although a few other minor parts also exist, we have highlighted only the major ones for the broad discussion providing very specialist technology in pockets.

- Payments as a Service (PaaS)

- Banking as a Service(BaaS)

- Insurtech as a Service (IaaS)

- RegTech as a Service (RaaS)

- Cybersecurity

- Wealthtech as a Services (WaaS)

- Blockchain

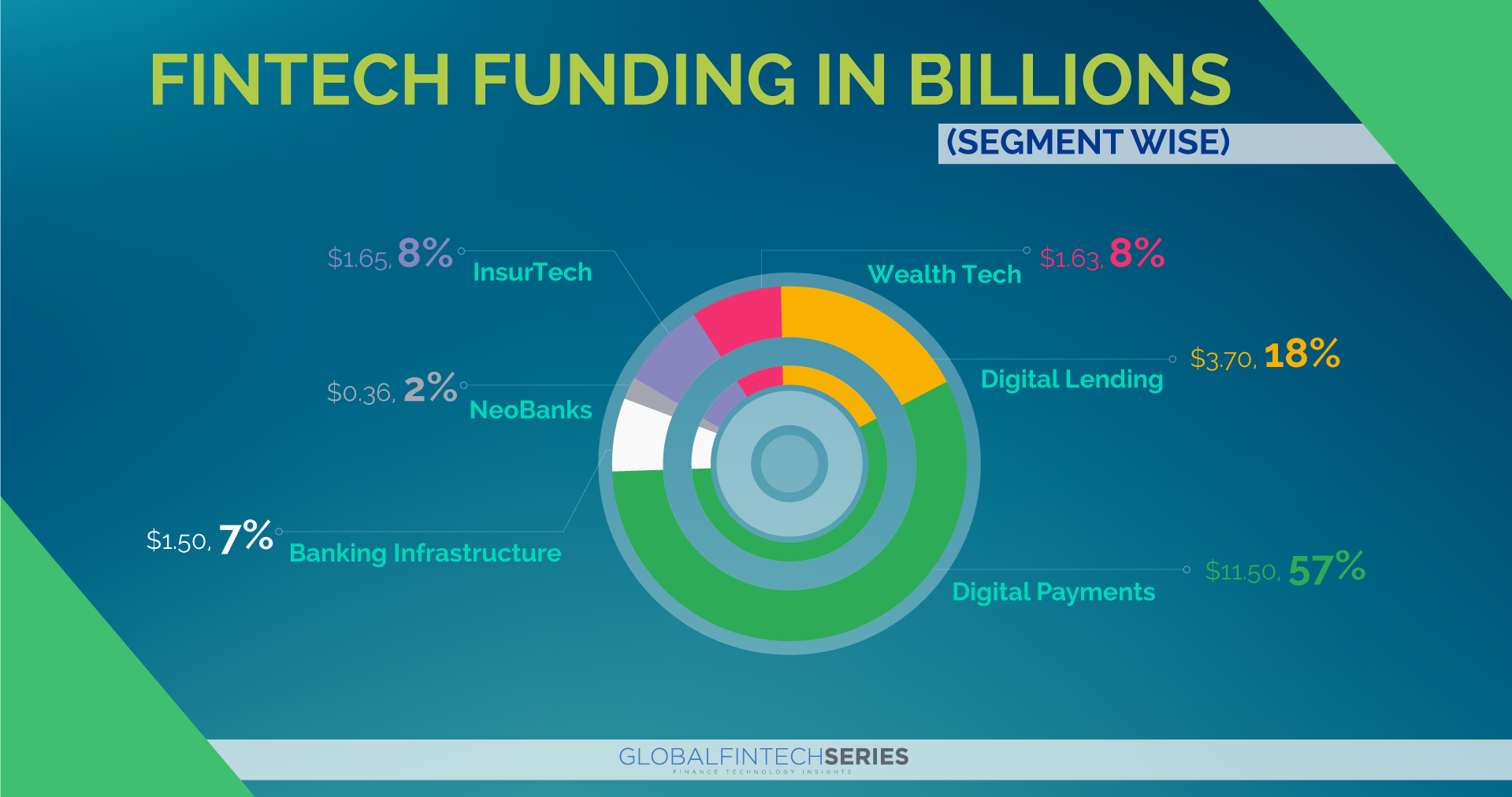

Below is the chart highlighting the Fintech funding across its varied components. Digital payments top the funding arena among all. As of September 2021, around 48.5 percent of FinTech companies in India belonged to the payments segment.

First Key FinTech Segment- Payment

Digital payments are done digitally, with no exchange of physical cash involved. Such a method, sometimes called an e-payment, is the transfer of value from one account to another where both the payer and the payee use a digital device like a smart phone, computer, or a credit, debit, or prepaid card.

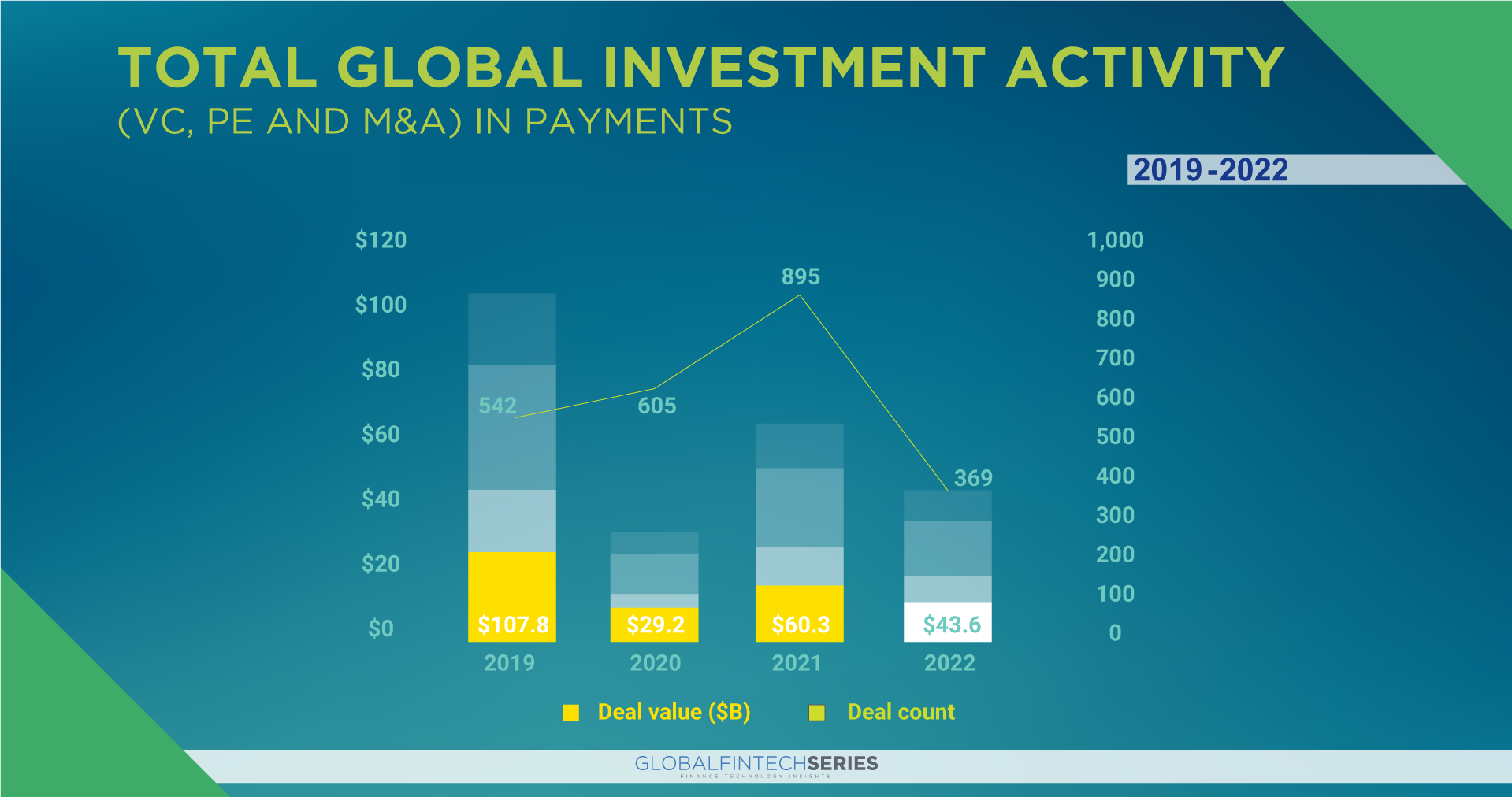

Investments were on a stronger sphere for 2022, accounting for $43.6 billion compared to $60.3 billion in 2021. The acquisition of Australia-based After paying by Block (formerly Square) for $27.9 billion accounted for the largest payments deal and globally the largest fintech deal followed by the $2.6 billion buyout of Bottomline Technologies by PE firm Thomas Bravo, and a $1 billion VC raise by UK-based Checkout.com.

Investments were on a stronger sphere for 2022, accounting for $43.6 billion compared to $60.3 billion in 2021. The acquisition of Australia-based After paying by Block (formerly Square) for $27.9 billion accounted for the largest payments deal and globally the largest fintech deal followed by the $2.6 billion buyout of Bottomline Technologies by PE firm Thomas Bravo, and a $1 billion VC raise by UK-based Checkout.com.

Read: What Is Machine Learning?

Second Key FinTech Segment- Banking-as-a-Service (BaaS)

Banking-as-a-Service refers to digitally providing banking services and products by non-traditional players (usually Fintechs) using third-party distributors. The global BaaS market size was valued at $2.41 billion in 2020 and is projected to reach $11.34 billion by 2030, growing at a CAGR of 17.1% during the period. Banking as a Service allows third-party organizations to draw off of the existing banking services through APIs that communicate between banks and third parties. These APIs allow the use of these banking services by fintech companies, programmers and developers, and other non-financial companies.

Besides, it stretches out its presence to non-banking players who wish to give banking offices to their clients packaged with their product offerings. It makes a solitary stage to empower a quicker and smoother go-to showcase for banking administrations. For example, when we buy a refrigerator from an e-commerce website, the checkout page will give instant lending services in addition to multiple options to make payments like BNPL. Banks are partnering with fintech companies to innovate financial services and BaaS will enable the ecosystem of a generic finance product. In this way, the eventual fate of Fintech exists in the development of BaaS and its connected items and administrations to a great extent. The digital transformation and mobile-first concept have risen and have had an extraordinary impact in affecting it.

Recommended: Demystifying AR/VR Technology In Healthcare Domain

Third Key FinTech Segment- Insurtech

Insurtech is a combination of Insurance and Technology which is the result of the convergence between digitization, disruptive innovation strategies, and the insurance sector. The recent application of innovative techniques such as AI, ML, or big data to the insurance sector, as well as the birth of startups, focused on offering this type of solution to create disruptive insurance products which gave an edge to the entire concept. The following are few advantages:

- Reducing costs in customer acquisition and onboarding.

- The possibility of expanding business globally, without borders.

- Automate customer acquisition while improving user experience.

- Offers products, services, contracts, and all kinds of procedures remotely and online.

- Improving security controls and fraud detection.

- Complying with the most demanding regulations regarding technical and legal security when acquiring new clients both in-person and online.

Its players include Damco Group, DXC Technology Company, Quantemplate, Acko, Digit, and Easy policy which are proliferating as the insurance market picks up the market heat of rising insurance policyholders although amid global uncertainty this sector experienced some slowdown as well.InsurTech companies take the help of cutting-edge technologies to build customer-centric insurance products and services such as digital insurance, bulk employee insurance products, insurance comparison platforms, etc. These services can be enabled by offering insurance infrastructure API, underwriting services, claims management, insurance product customization, and policy management system-related services.

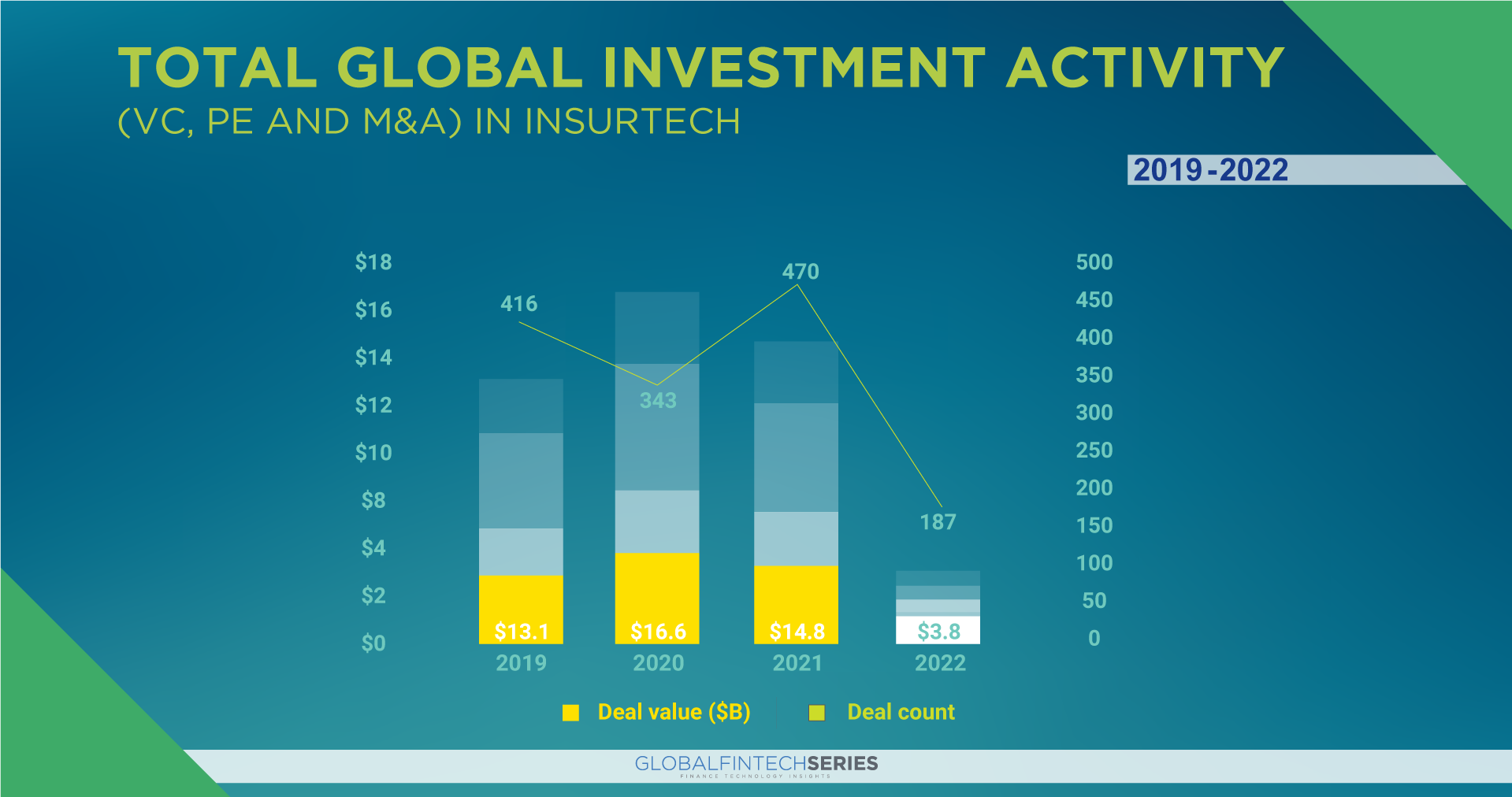

Investment in the insurtech sector dropped impressively, with $3.8 billion of investment globally in 2022 while $14.8 billion investment was seen in 2021. The biggest insurtech arrangement of this current year was the securing of US-based Zenefits by TriNet for $220 million. This was trailed by several $100 million+ VC deals, including $211 million and $200 million raises by Healthcare.com and New front insurance both in the US, and a $196 million raise by France-based Alan. The Americas and Europe represented by far the most insurtech around the world.

Investment in the insurtech sector dropped impressively, with $3.8 billion of investment globally in 2022 while $14.8 billion investment was seen in 2021. The biggest insurtech arrangement of this current year was the securing of US-based Zenefits by TriNet for $220 million. This was trailed by several $100 million+ VC deals, including $211 million and $200 million raises by Healthcare.com and New front insurance both in the US, and a $196 million raise by France-based Alan. The Americas and Europe represented by far the most insurtech around the world.

Fourth Key FinTech Segment-Regtech

{kind=link}

RegTech as a Service (RaaS) encourages FIs to see RegTech as a way to improve working processes for efficiency as well as regulatory compliance. A subset of fintech that spotlights innovations that might work with the conveyance of administrative prerequisites more productively and really than existing capabilities. Regulation innovation organizations use innovation to ease clients’ consistency to guarantee insignificant resistance and smoothed out client onboarding processes. RegTech organizations offer KYC and ID check administrations, charge consistency, computerized onboarding, AML consistence, misrepresentation discovery instruments, and hazard the executive’s devices and programming that share the consciousness of the administrative necessities and assist them with conforming to those prerequisites easily.ClearTax, EaseMyGST, and Khata Book are driving the RegTech area by offering different consistency-related administrations.

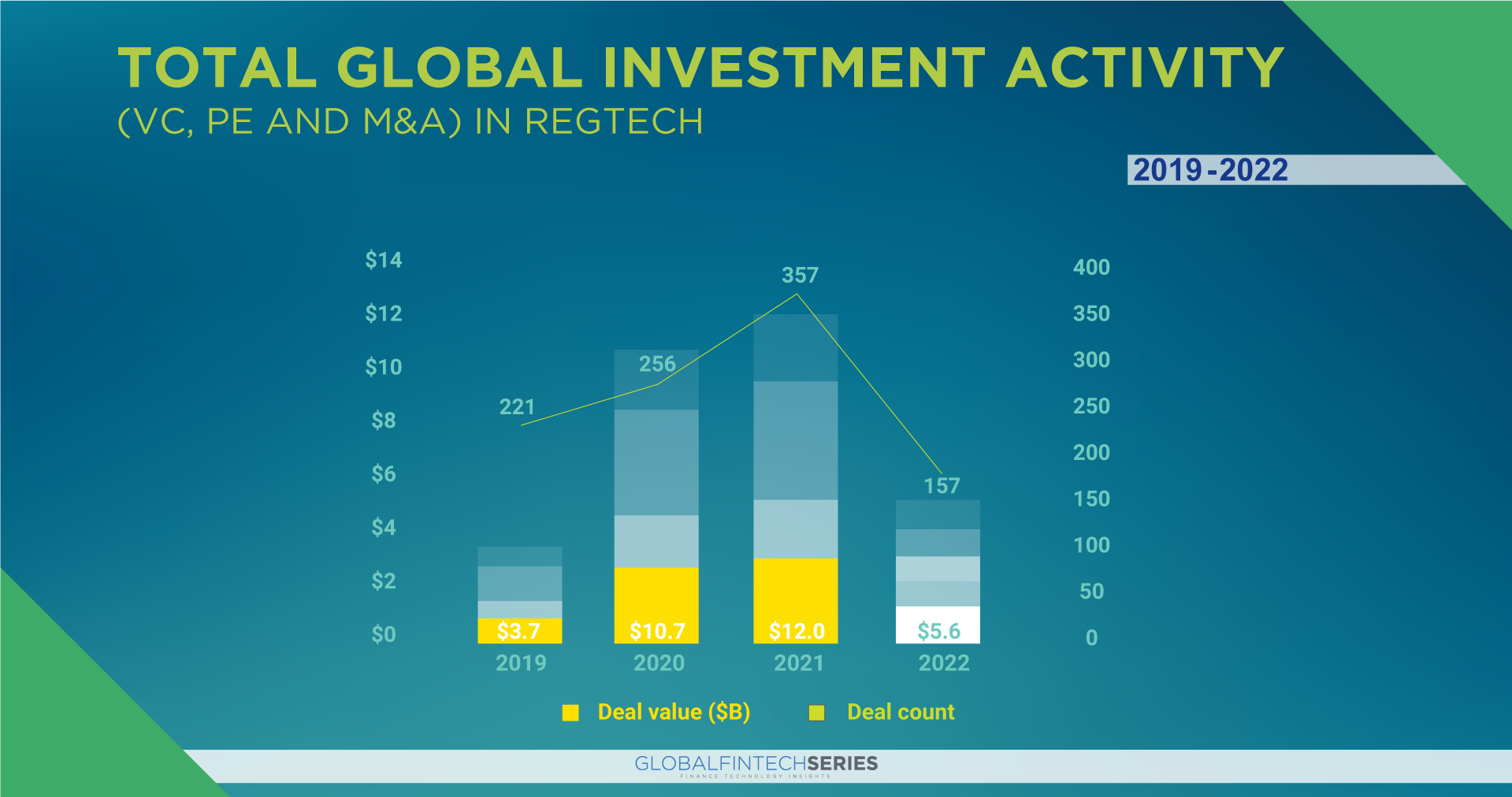

Key companies in the Global RegTech Market incorporate ACTICO GmbH, Broad-ridge Financial Solutions, Inc., Deloitte Touche Tohmatsu Limited, Jumio, MetricStream Inc., NICE, PwC, and Thomson Reuters.Regtech companies pulled $5.6 billion in investment globally. The US accounted for the largest portion of regtech investment, including the $2.6 billion buyout of Bottomline Technologies by Thomas Bravo, the $450 million Series D raise by ConsenSys, and the $240 million acquisition of FourQ by cloud-based financial operations organization Blackline.

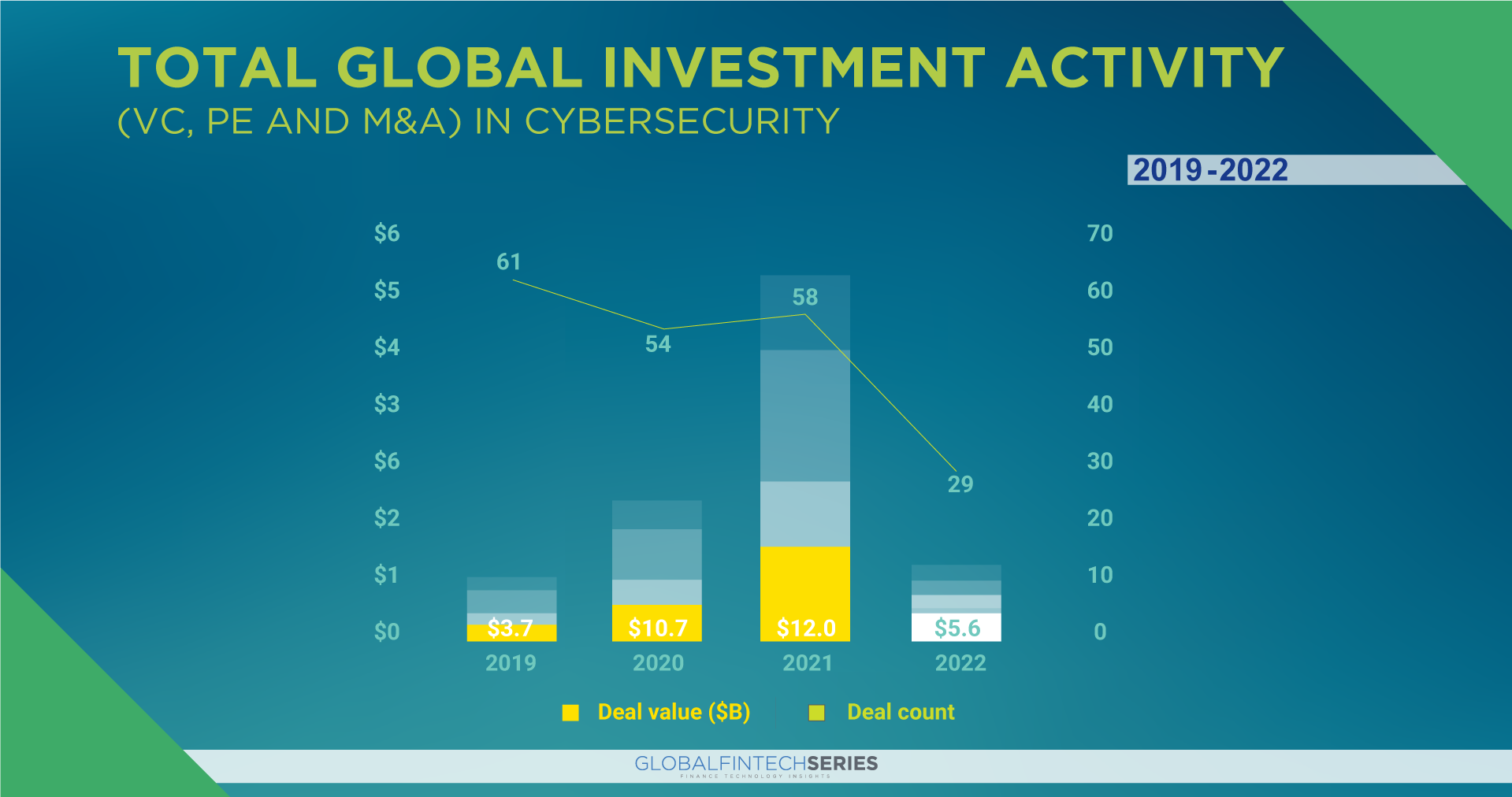

Fifth Key FinTech Segment- Cybersecurity

Online protection isn’t just about overseeing risk, likewise, an essential issue shapes item capacity, hierarchical viability, and CRM. Cybersecurity has forever been a ceaseless race, yet the pace of progress is speeding up. Organizations are proceeding to put resources into innovation to maintain their organizations. Presently, they are layering more frameworks into their IT organizations to help remote work, upgrade the client experience, and produce esteem, all of which makes potential new vulnerabilities. Cybersecurity space major areas of strength stayed by four major raises in the US, including a $550 million raise by Fireblocks, a $170 million raise by Chainalysis, and a $100 million raise by TokenEx and Cowbell Cyber. Estonia-based Veriff also raised $100 million in 2022. In March 2022, Google announced plans to acquire incident response company Mandiant for $5.2 billion, highlighting the immense focus that hyper-scale providers are placing on cybersecurity automation and platform solutions. Whenever finished, the arrangement would break worldwide records.

Online protection isn’t just about overseeing risk, likewise, an essential issue shapes item capacity, hierarchical viability, and CRM. Cybersecurity has forever been a ceaseless race, yet the pace of progress is speeding up. Organizations are proceeding to put resources into innovation to maintain their organizations. Presently, they are layering more frameworks into their IT organizations to help remote work, upgrade the client experience, and produce esteem, all of which makes potential new vulnerabilities. Cybersecurity space major areas of strength stayed by four major raises in the US, including a $550 million raise by Fireblocks, a $170 million raise by Chainalysis, and a $100 million raise by TokenEx and Cowbell Cyber. Estonia-based Veriff also raised $100 million in 2022. In March 2022, Google announced plans to acquire incident response company Mandiant for $5.2 billion, highlighting the immense focus that hyper-scale providers are placing on cybersecurity automation and platform solutions. Whenever finished, the arrangement would break worldwide records.

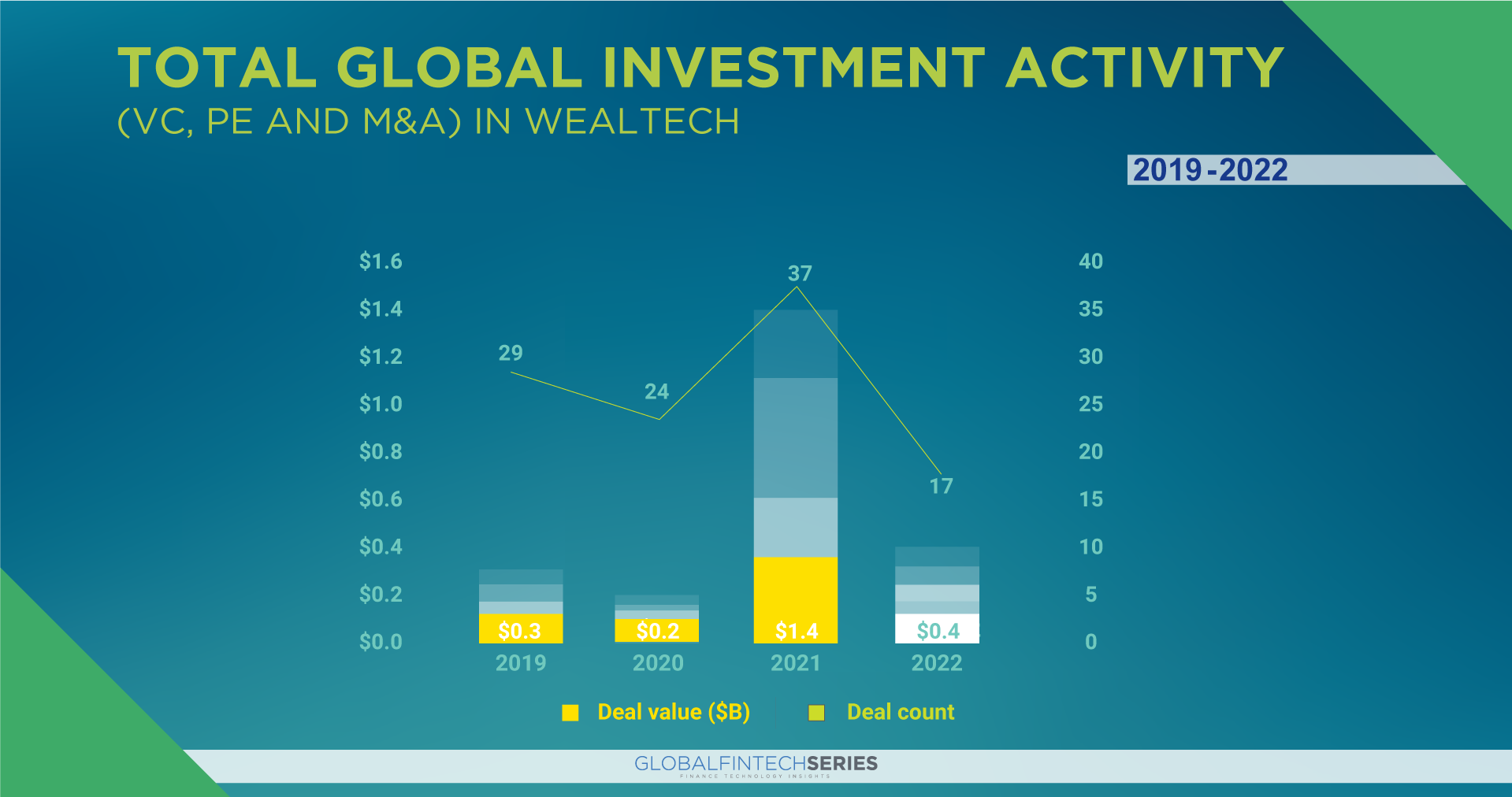

Sixth Key FinTech Segment- Wealth tech (WaaS)

Digital portfolio management, Wealth-as-a-Services, embedded wealth, digital broker, Robo retirement, and white-label Robo advisors are some of the most prominent areas of WealthTech companies.

Digital portfolio management, Wealth-as-a-Services, embedded wealth, digital broker, Robo retirement, and white-label Robo advisors are some of the most prominent areas of WealthTech companies.

Internationally, abundance tech pulled in $443 million during 2022, driven by US-based Titan’s $100 million VC subsidizing round, and UK-based MoneyFarm’s $59.8 million arrangement. The developing development of the wealthtech area has driven financial backers to take a more basic perspective on open doors. They are presently zeroing in less on making wide speculations across the space, focusing their capital on abundance specialists with USP business models and those seen to be more important, vigorous, and monetarily feasible contrasted with their companions. Model, Blockchain.com declared its procurement of Singapore-based exchanging centered Independence, while advanced resource stage Golden Gathering reported its securing of Hong Kong (SAR), China-based resource the board firm Celera Markets. Proceeded with the development of crossover abundance warning models which zeroed in on giving innovation stages.

Read: 5 Unconventional Ways To Make Money On Crypto In 2023

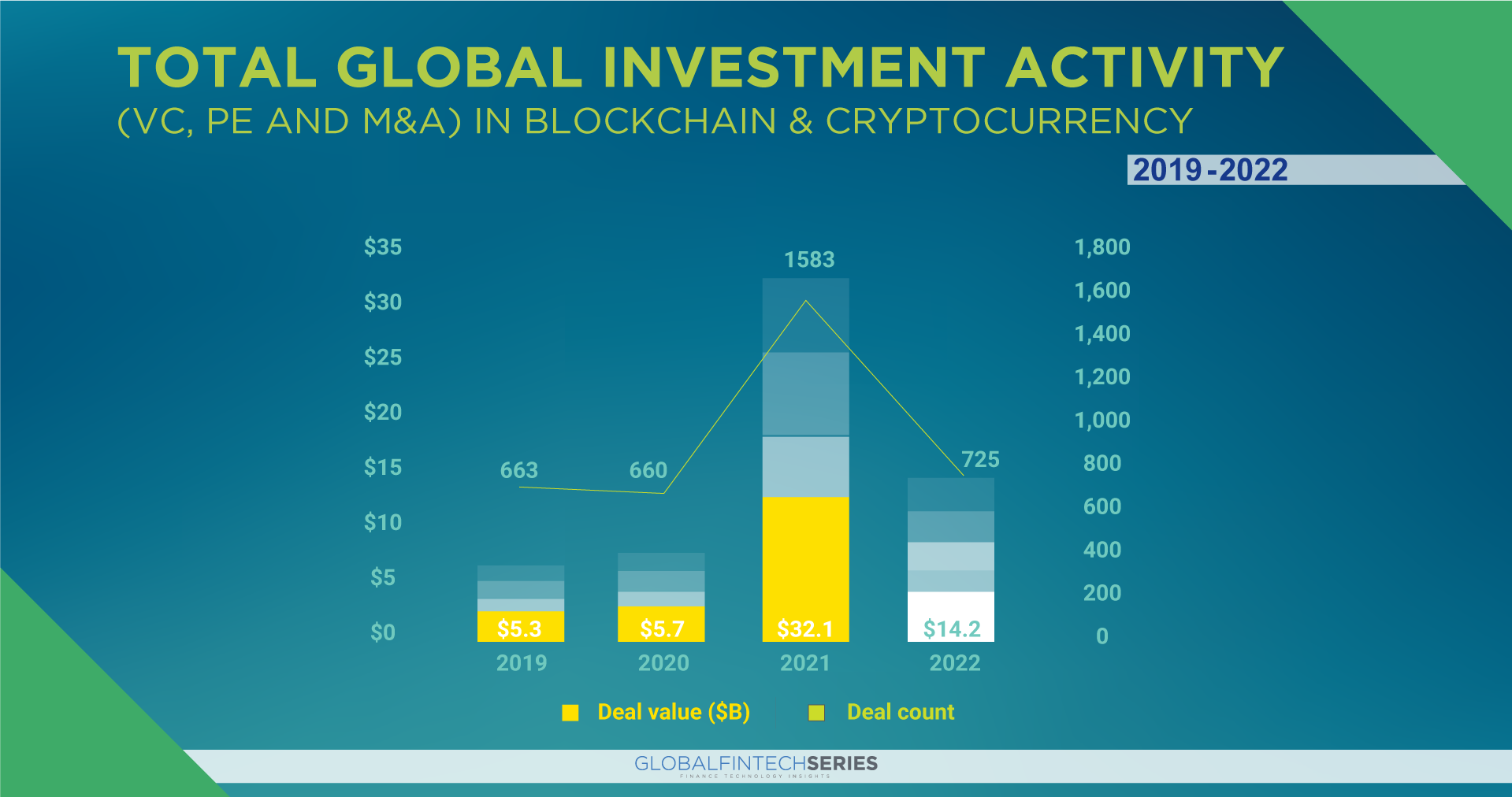

Seventh Key FinTech Segment- Blockchain/Cryptocurrency

Blockchain innovation is a decentralized, circulated record that stores the record of responsibility for resources. Any information put away on the blockchain can’t be changed, making the innovation a genuine disruptor for ventures like payments, cybersecurity, and healthcare. Find more about what it is, how it’s used, and its history. Investment in crypto and blockchain falls from 2021 high and remains ahead of all other years. After a record-shattering 2021, global investment in crypto and blockchain fell to $14.2 billion in 2022. In spite of the crypto space imploding because of the startling Russia-Ukraine struggle, rising expansion, and the difficulties experienced by the Terra crypto ecosystem, investment at mid-year stayed well over the entire years before 2021. This features the developing development of the space and the broadness of innovations and arrangements drawing in the venture.

One of the largest deals came from VC raises, including a $1.1 billion raise by Germany-based Trade Republic, a $550 million raise by US-based Fireblocks, a $500 million raise by Bahamas-based FTX, and a $450 million raise by ConsenSys. Prior to 2018, most crypto investments came from retail consumers. The current macroeconomic trend will likely be an important test for cryptos, and especially Bitcoin, in terms of correlation with other assets. While China has banned crypto trading outright, and India is considering following suit, the regulators in a number of other jurisdictions have continued to focus on finding ways to protect consumers while also fostering the evolution and growth of competitive and attractive crypto markets. Since then, the investor profile has changed, with institutional and corporate investors now accounting for a much larger share of investment.

The Key Line

Each segment contributes to the Fintech Verse independently on a global platform with its counterparts. Tech-savvy legacy banks that create their own BaaS Market stages presently won’t just stretch out beyond the open financial open door before their rivals, yet in addition, open another surge of income by adapting their platforms. The Fintech scene around the world will overwhelmingly be driven by the PayTechs, LendTechs, and WealthTechs, which are firmly interconnected with BaaS. Hence, the eventual fate of Fintech is Banking-as-a-Administration and the forthcoming digital banking ecosystem enablers.

Read: Did You Know- 14 Bitcoin Facts

[To share your insights with us, please write to sghosh@martechseries.com]