Pooja Choudhary

Banking as a Service (BaaS) is one of the fintech innovations that has empowered the collaboration of banks with fintech. The computerized change and mobile-first approach that has risen above the recent years plays an extraordinary role in affecting BaaS. A BaaS platform offers clients the chance to pick the necessary financial products and services and use them as per their requirements.

What Is Banking As A Service (BaaS)?

BaaS is the provision of banking products and services through third-party distributors. Through integrating non-banking businesses with financial infrastructure, BaaS offerings are enabling specialized interfaces and bringing them to market speedily. Simply put, non-bank businesses offer banking services without having to launch or acquire their own bank. BaaS is an end-to-end approach that facilitates fintech and other third-party organizations to connect with a bank’s tech system employing APIs. This helps the organizations build innovative financial services upon the provider bank’s regulated infrastructure while enabling open banking services. The banking sector has gone through somewhat of a metamorphosis in the last few years. With fintech players entering the market, this transformation has become unstoppable. Financial services are changing in a way that they’re creating new products, channels, partnerships, and opportunities. Banking as a Service plays a significant role in this sphere.

Read: 5 Unconventional Ways To Make Money On Crypto In 2023

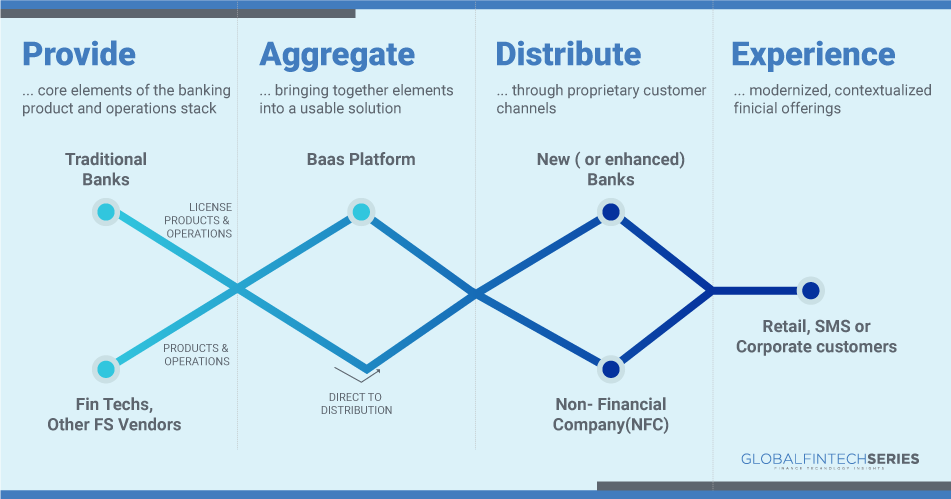

How Does The BaaS Value Chain Work?

Banks are trying to catch up to the speed of fintech companies. Or, banks are partnering with fintech companies to innovate financial services. Banking as a Service allows third-party organizations to draw off of the existing banking services through APIs that communicate between banks and third parties. These APIs allow the use of these banking services by fintech companies, programmers and developers, and other non-financial companies. This allows them to build their own features as a layer on top of the existing banking services.

Read: Did You Know- 14 Bitcoin Facts

Here’s a detailed breakdown of the 3 layered, API-based Banking-as-a-Service stack:

- The bottom level represents the traditional, nationally-chartered financial institution (bank) that partners with the BaaS provider — also known as the “Infrastructure-as-a-Service (IaaS) layer.”

- The middle represents the “Bank-as-a-Service layer” that maps out banking services personalized as an ecosystem for FinTech startups, and delivers its products and services to end users. This part of the stack sends data back and forth between the bank and FinTech, through the BaaS provider as an intermediary.

- The top layer is the FinTech company that interfaces with the end user which receives data from customers and forwards it to the BaaS layer on the transaction request. The BaaS provider also sends data from the bank to FinTech as responses to transaction requests.

BaaS Statical Analytics:

- 30% of customers are considering switching banks

- 42% of customers have used a Buy Now, Pay Later service

- 2x ROAA for banks focused on BaaS offerings (done till here)

Recent Examples Of BaaS:

Multiple fintech platforms such as Dave, SoFi, and Betterment have launched deposit accounts as an add-on product to their initial core offering powered by white-label BaaS providers or bank partnerships. Top companies and what they offer Synapse (deposit accounts, loans, card programs, crypto, payments), Cambr (deposit accounts, debit cards, payments), Bankable (digital banking, card programs, e-wallets), Treezor (payments), GreenDot (deposit accounts, card programs, payments).

Traditional Vs New Age Banks

Below is the graphical representation, we can easily differentiate between the traditional and new-age banks.

{kind=link}

Benefits of BaaS For Fintech And Non-fintech Companies

- Low cost: For a financial institution, BaaS is an opportunity to reach a greater number of customers at a lower cost. The traditional banking model is based on expensive legacy technology and operations. The cost of acquiring a customer is typically in the range of $100 to $200.With a new, greenfield BaaS technology stack, the cost can range between $5 and $35.

- Online Banking: They may concentrate on improving their offerings rather than worrying about bank licenses and integrations. For their customers, these user-friendly and technologically advanced products may be a better option than traditional banking. They can also design apps for their consumers to keep track of their daily transactions, account balances, and savings. Surprisingly, all of this is made feasible by simple APIs.

- Offer Debit and Credit Cards: Non-banks can offer credit and debit cards to their consumers using the Banking as a Service (BaaS) paradigm. Consider the Apple Credit Card. Through an app, customers may obtain real-time updates on all of their transactions. The account information and payments for the customer are shown in a user-friendly manner.

- Offer Loans: Businesses can also use BaaS to lend money to their clients. Furthermore, companies can provide customers with Buy Now, Pay Later choices. The customer has the option of choosing their payment schedule in advance. They might use an app to keep track of their monthly EMI payments.

- Investment Services: Here they assist customers and automate their finances and invest their assets. They can assist customers in creating customized investment plans using low-cost index funds. They can also automatically rebalance the portfolio in accordance with the customer’s investment strategy.

- Verify the customer’s identity: Failures in payment transfers might jeopardize an organization’s reputation. Furthermore, it is possible that a company’s merchant account will be labeled as a “high-risk merchant.”Payment transfer failures can be reduced with bank account verification.

What Are The Benefits Of Implementing The BaaS Model?

- Expanded Income Streams: BaaS empowers banks to impart information to third-party financial institutions through APIs. BaaS gives new income sources to banks as open banking turns into the norm. In reality, 43% of banks need to work under a model that licenses them to charge a fee each for each transaction. Fintech and IT firms are on the ball concerning development and speed. Banks, on the other hand, have the trust of their customers and a vast amount of funding capacity at their disposal.

- Drive to Save Money: Banks can benefit from BaaS not only in the context of income generation but also regarding cost reduction. Banks are not expected to put resources into technological advancement. As an outcome, they might benefit from third parties since they as of now have instant arrangements. In actuality, this can help banks in making extra ventures and earnings. It’s no surprise that 77% of banks need to put resources into open financial endeavors for their corporate clients.

- Increased Client Experiences: When a bank works with a third-party supplier, it acquires additional consumers. They tend to find out about the inclinations and taste patterns of their clients. For instance, their buying propensities and monetary needs. Banks can now use this gathered data to create custom-made offers for their purchasers. All things considered, individualized offers are bound to be acknowledged by 80% of clients. They can likewise utilize a more designated multi-channel showcasing approach. This might help organizations in diminishing their dependence on over-the-line spending.

Read: Cybersecurity Timeline and Trends You Should Know before Planning for 2023

Advantages Of BasS For End-Customer

BaaS promotes financial services competition by allowing non-banks to provide fundamental banking services. As a result, innovation is pushed forward, and customers have access to more user-friendly products. Furthermore, it leads to increased financial transparency. Customers’ individual pain areas are the focus of third-party players. For example, a fintech company may solely specialize in business payouts. This pressure has simply started to ascend as increasingly more technology businesses enter into the banking sphere. The client demographic is one more feature of this issue. The new consumer base is technologically sophisticated and expects real-time access to financial data and products. To our surprise, the nations with a youthful populace had the best fintech adoption rate. The frequency may be essentially as high as 50%. However, getting to that phase of client satisfaction is a tremendous achievement all by itself. All things considered, interfacing with a bank and creating financial products on top of that requires severe information security and consistency protocols.

Read latest article: What Is Data Science?

Challenges Faced By BaaS

- Traditional banking institutions are gradually losing the “customer trust” edge they once held over participants in the fintech industry Given that tech trends for CIOs and CTOs are not being followed. On the other side, numerous technology businesses are expanding their operations into the financial sector because of the high levels of client trust they have earned ( Eg. Apple Card).

- New associations can mean new risks, and financial institutions should deal with these cautiously. A partnership governance model will be fundamental to characterize plainly the jobs and obligations of the monetary foundation and the wholesaler. The model ought to remember a clear arrangement for revenue split, well-laid-out processes, and performance monitoring.

- In addition to this, BaaS requires working together with several third-party players. The functional capacities naturally share a lot of similarities with one another. In addition, many businesses offer their products under a white label, which is another term for private labeling. This may lead to confusion among final customers.

- Looking closely at these contemplations, the fate of BaaS uncovers a huge change in the obligations of the players. There is a possibility that banks will change from the capability of “makers” to “assemblers” This demonstrates that they won’t confine their attention to the primary banking services they offer. All things considered, monetary establishments will collect value-added services out of the administrations given by their business partners.

Futuristic View For BaaS

The future of BaaS will be a considerably more mature, refined, and enhanced rendition of what we see today. The meaning of BaaS will be parted into numerous subcategories with new market participants, particularly enormous tech giants that have been remaining uninvolved. In the following couple of years, the business will develop to become straightforward as firms and controllers will cooperate to bring all banking services by means of API. Overall, the Banking-as-a-Service sector will accomplish standard reception in the following 10 years as consumers request the best from financial services providers. Players inside BaaS will begin to cover as banks become more “FinTech-like” and fintech constructs similar financial capacities from a less controlled scene. The new competition will come from tech giants that have laid out client groups that might benefit from a similar brand of innovation. Risk and controls will evolve to protect critical customer data but allow for a smoother process for identity verification across multiple companies and services. Consumers will consolidate their deposit balances with organizations that can convey a full ecosystem of financial services adaptable to their progressions throughout everyday life. Notwithstanding if banks, fintech, tech giants, or some hybrid mix of these organizations are delivering the solution. Banking-as-a-Service will keep on making banking generally accessible to any organization capable of delivering valuable services to customers or market segments around the world.

Banking as a Service (BaaS) is reconfiguring the banking value chain, opening the door to disintermediation and enabling new sources of growth. BaaS is the provision of banking products and services through third-party distributors. Through integrating non-banking businesses with regulated financial infrastructure, BaaS offerings are enabling new, specialized propositions and bringing them to market faster. Also, a BaaS business is scalable and agile, making it particularly suitable for entering new markets and then expanding.

[To share your insights with us, please write to sghosh@martechseries.com]